What is a 1031 exchange? | Like-kind property | Why use one? | Rules & requirements | Qualified intermediaries | How it works | Case study | Tips | FAQs

With a 1031 exchange, property owners can "swap" one investment or business property for another of equal or greater value while deferring capital gains tax and avoiding depreciation recapture — essentially leveling up their equity without having to pay a steep tax bill.

The 1031 exchanges get their name from the Internal Revenue Code Section 1031, which outlines how they can be used.

1031 exchanges can save real estate investors and business owners thousands of dollars, but they are confusing. Given all of their rules and regulations, they aren’t beneficial in every situation.

In this guide, we’ll get into everything that you need to know about 1031 exchanges, but you should definitely consult an accountant or tax professional before starting an exchange.

What is a 1031 exchange?

In a 1031 exchange, the owner of an investment or business property exchanges one property for another. The replacement property is generally of equal or greater value.

When you exchange a property, any capital gain that you’d normally incur is passed on to the next property, so you won’t have to pay taxes until the replacement property is sold.

This means a 1031 exchange can be used to defer taxes, not avoid them forever. It’s an economic incentive — not a tax loophole.

The IRS allows 1031 exchanges because they incentivize real estate investors and business owners to scale up their business by buying larger, more valuable properties.

For a 1031 exchange to be valid, a qualified intermediary must hold onto the proceeds of the sale until the money can be transferred to the seller of the new property.

To report the exchange to the IRS, you need to file Form 8824 with your tax return.

What is a like-kind property?

Any property that is exchanged in a 1031 exchange must be "like-kind." So what does that mean, exactly?

According to the IRS, "like-kind" means that the properties are of the same nature or character, not necessarily the same grade or quality.[1]

For example, one apartment building could be exchanged for another — even if the two buildings are very different in terms of their value, condition, features, etc.

To take it a step further, you could even sell a vacant piece of commercial land and exchange it for an office building since both are real estate.

Any property that’s located outside of the United States cannot be considered "like-kind" to property that is located within the U.S.

While finding a "like-kind" property can place some limits on your 1031 exchange, there’s actually more leeway here than most people realize, so "like-kind" can be a misleading phrase.

|

What is the "boot?" "Boot " or "mortgage boot" is a term that is commonly used in the context of 1031 exchanges. It’s not a technical term that the IRS uses, but it’s a reference to any cash received in the exchange that is not reinvested in the replacement property. One way that this may occur is if the mortgage for the new replacement property is less than the mortgage that was paid off when the original property was sold. For example, if the balance of the mortgage on the original property was $100,000 at the time that you sold, and the mortgage that you needed for the replacement property was only $80,000, the "boot" would be $20,000. This reduction in debt is viewed as a taxable cash benefit that will be taxed as a capital gain. |

Why would you use a 1031 exchange?

There are three important reasons why a smart business person or real estate investor would use a 1031 exchange:

Defer capital gains

The primary reason for using a 1031 exchange is to defer payment of taxes on your profits. Typically, when you sell a property, you’re taxed on your capital gain in the sale —the difference between what you paid for the property and what you sold it for.

Capital gains tax can add up quickly, particularly if you’re selling a valuable property or a property that has greatly appreciated in value while you’ve owned it.

Capital gains consist of Federal and state taxes, but there's also depreciation recapture (which we'll talk about in a minute) and Net Investment Income Tax (NIIT) of 3.8% which can come into play if you're income is above the IRS threshold.

For now, let's look at capital gains since this makes up the largest portion of taxes in most real estate transactions.

If you purchase a four-unit residential property in California for $250,000 and then sell it ten years later for $400,000, you will have a capital gain of $150,000.

But let's say you've claimed $30,000 of depreciation over the ten year period, and you have eligible closing costs of $5,000. Given these assumptions, your actual gain is $175,000.

When we crunch the numbers and add up Federal capital gains tax (15%), California capital gains tax (13.3%), and depreciation recapture (25%), you're on the hook for $52,525!

But, with a 1031 exchange, you could defer that hefty tax bill by acquiring a replacement property of equal or greater value.

» READ: Understanding Capital Gains Tax on Real Estate Investment Property

|

In some cases, you may never pay capital gains at all! When the replacement property from a 1031 exchange is sold, capital gains tax is calculated using your original deferred gain, plus any additional gain that has been realized since you purchased the new property. However, there’s one exception to this rule. If you die before selling a property that was acquired in a 1031 exchange, the government will forgive the capital gains tax. This means that, theoretically, you could perform several 1031 exchanges in your lifetime to increase the value of your investment property, without ever paying capital gains tax! For this reason, 1031 exchanges have interesting estate planning possibilities. We’re not tax professionals, so make sure you talk to an accountant to find out if a 1031 exchange makes sense for you. |

Avoid depreciation recapture

Landlords are allowed to record depreciation in the value of their investment properties to offset their income tax.

In reality, most properties appreciate in value over time, but because an investment property is a business asset, depreciation is allowed because it’s assumed that there will be wear and tear from tenants.

However, when you go to sell an investment property and there’s a gain, the depreciation that you recorded during your years of ownership gets "recaptured" by the IRS — meaning that the total depreciation you recorded is taxed.

To sidestep depreciation recapture, some landlords use a 1031 exchange so that they can build their portfolio without getting hit by the depreciation that they’ve been benefiting from for years.

Depreciation recapture will eventually come into play if the replacement property is sold.

Leverage equity

By exchanging a property that you already own for one (or several) that could increase your cash flow, you’re essentially "leveling up" your investment.

Every new purchase has a cost, but by filing for a 1031 exchange, you can minimize the cost and possibly improve your upside.

1031 exchange rules and requirements

There are three rules for identifying a property or properties as a replacement in a 1031 exchange. You don’t have to meet the requirements of all three rules. Instead, you have to choose one rule and follow it.

Identifying properties for a 1031 exchange

|

Rule |

How it works |

Best for... |

|---|---|---|

|

The 3-property rule |

The owner identifies three properties to replace the property being sold, but only has to close on one of them. Because this rule is easy to use and relatively low-risk, it’s the one that’s used the most. |

Exchanging one property for another. |

|

The 200% rule |

The owner can identify an unlimited number of properties to replace the one being sold, but their cumulative value can’t exceed 200% of the original property’s value. |

Exchanging one property for multiple properties. |

|

The 95% rule |

With this rule, the owner can identify an unlimited number of replacement properties with no maximum value, but they must close on at least 95% of their cumulative value in order to qualify for a 1031 exchange. This rule is rarely used because it’s so difficult to exercise and carries the most risk. |

High-value transactions where an investor is making a major jump in value of their investment portfolio. |

It’s important to remember that no matter which rule you choose to follow, the exchange will be voided if you receive any of the proceeds from the sale of the first property. The funds have to be transferred directly to a qualified intermediary and held until a new property is purchased.

Using a qualified intermediary

A qualified intermediary is a non-related third party who’s responsible for holding onto the money from the sale of one property until it’s used to purchase another property.

You can’t have a valid 1031 exchange without a qualified intermediary.

But who can act as a qualified intermediary? There is no official license or certification that is mandated by the IRS.

What’s most important is that the qualified intermediary is a third party with whom you have no previous relationship.[2]

A qualified intermediary could be an:

- Attorney

-

Investment banker

-

Professional QI service

Any person who has acted as your "agent" — a broad term for any kind of professional representation — within the last two years is automatically disqualified from being your intermediary.

To ensure that your exchange isn’t voided by the IRS because of a potential conflict with the intermediary, it’s best practice to work with someone who you’ve never had any business dealings with in the past.

The more impartial and distant that third party appears to be, the better.

How a 1031 exchange works

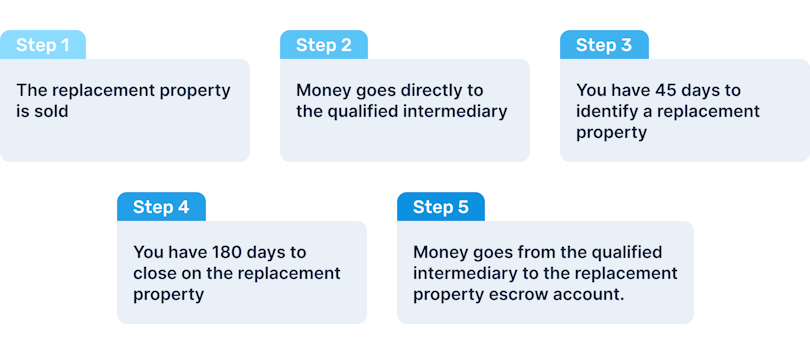

In a delayed or deferred 1031 exchange, the first property is sold, a new property is identified, and then the exchange takes place at the time of closing.

-

The replacement property is sold. You must specify when you’re selling the property that you’re going to do a 1031 exchange. That way, when you sell there’s no chance that the money will be sent directly to you.

-

Money goes directly to the qualified intermediary. You can’t accept the proceeds from the sale and then pass them along to the qualified intermediary — they have to go directly to the QI or the exchange will not be valid.

-

You have 45 days to identify a replacement property. 45 days is a short window of time, but that’s all that the IRS gives you to identify a property or properties that will be the replacement in your exchange.

-

You have 180 days to close on the replacement property. The 180 period starts on the day that the sale of the original property closes and ends when you close on the replacement property. If the deal takes any longer than that, the exchange is invalid.

-

Money goes from the qualified intermediary to the replacement property escrow. This completes the qualified intermediary’s involvement in the 1031 exchange process and ensures that you do not receive profits from the sale at any point along the way. Money is held in escrow, a third-party account, until the deal closes.

Because a 1031 exchange can cost anywhere from $450 to $1,500,[3] it might not be worth it if you have little to no realized capital gains on the property.

Before you enter into this process, you should consult an accountant or tax professional to make sure that a 1031 exchange is possible and beneficial in your situation.

Exchange expenses

A 1031 exchange comes with closing costs, just like a normal real estate transaction. Closing costs include things like title insurance premiums, property taxes, and attorney’s fees.

Some closing costs in a 1031 exchange are considered to be exchange expenses — meaning that funds from the exchange can be used to pay them.

Paying non-eligible expenses using funds from the exchange could void the entire 1031 transaction.

|

Eligible exchange expenses |

Non-eligible exchange expenses |

|---|---|

|

|

A 1031 exchange case study

|

Clever’s very own CEO and Co-founder Ben Mizes did a 1031 exchange to purchase his second investment property; an 18-unit apartment building. At the time, Ben owned a fourplex but wanted to move up to a larger investment in order to improve his cash flow. The problem? He had enough cash to cover the down payment, but not the taxes. Using Asset Preservation Incorporated as a qualified intermediary, Ben did a 1031 exchange of his fourplex for the 18-unit facility. As a result, his monthly gross rental income went from $2,800 to $11,000 and he was able to defer over $25,000 in taxes! |

Other types of 1031 exchanges

Besides a delayed exchange, which is the most common, a 1031 exchange can happen in a number of other ways.

-

Reverse exchange: The replacement property is purchased before the original property is sold.

-

Simultaneous exchange: The replacement property is purchased at the same time that the original property is sold.

-

Improvement exchange: Proceeds from the sale are used to renovate/improve the new investment. This type of exchange can even be used to build a new building.

-

Personal property exchange: Rather than exchanging real estate, ownership of personal property like machinery and equipment is exchanged.

-

Delaware Statutory Trust exchange: This option can be used to exchange full ownership of an investment for fractional ownership in a much larger investment.

1031 exchange tips

|

📅 Plan ahead: In a 1031 exchange, everything has to happen within a short window of time. You need to identify a replacement property within 45 days of selling, so research the market and pinpoint ideal replacement properties before you sell. 🤫 Don’t tell the seller it’s an exchange: If the seller is aware that you’re doing a 1031 exchange, they may be less likely to budge from their asking price because they know you’re on the clock. Don’t disclose to anyone on the seller’s side that you’re doing a 1031 exchange, or you might lose some serious leverage. You’re not legally required to tell the seller that you’re doing a 1031, so you’re not breaking any rules here. ⏱️ Give yourself extra time to close: You have 180 days to close on the replacement property. That sounds like a lot of time, but unexpected issues before closing can delay things. Pick a closing date that’s well within the 180 window so you don’t run out of time. |

Conclusion

When the numbers make sense, 1031 exchanges can be a great way to leverage equity and continue to build your investment property portfolio or scale up the assets in your business.

Successfully navigating a 1031 exchange could also save you thousands of dollars in capital gains taxes, keeping more money in your pocket for other business expenditures.

However, because the rules and regulations surrounding 1031 exchanges can be confusing, make sure you talk to an accountant and get their advice on how to proceed.

FAQs

How much does a 1031 exchange cost?

Qualified intermediaries generally charge a fee that can be anywhere from $450 to $1,500 for a 1031 exchange.[3] The median price is $750.

Are there any risks with a 1031 exchange?

There are some risks, such as:

-

The possibility that you won’t be able to identify the right replacement property with 45 days, or that your closing on the new property will not take place within 180 days.

-

The possibility that at some point during the process, the proceeds of the sale will end up in your possession — effectively voiding the exchange.

-

The possibility that the seller of the replacement property will back out of the sale, which would prevent you from completing the exchange.

How long does a 1031 exchange take?

A 1031 exchange cannot take any longer than 180 days from the date you sell your old property to the date that you close on the replacement property. However, the process could be much faster if you’re able to identify and close on a new property quickly.

Can you use a 1031 exchange to purchase a primary residence?

No — the purpose of a 1031 exchange is to exchange properties that are used for business or investment purposes. Primary residences are not included.

Can you have a mortgage in a 1031 exchange?

Yes. The profits from the sale of the first property can be used to pay off the remaining principal on the mortgage, and a new mortgage can be secured for the replacement property.