Are 'we buy houses' companies a rip-off? | What real customers say | 'We buy houses' scams | Other red flags to watch out for | How to protect yourself | Is selling to a cash buyer ever a good idea? | Alternatives | FAQ

💡 Key takeaways

- "We buy houses" companies aren't necessarily a rip-off — but they do make money by buying low and selling high.

- For sellers with hard-to-sell properties, an offer from a legitimate "we buy houses" company might be a good option.

- Cash-buying scams do exist, so look out for offers that come out of the blue from individuals or entities whose identity you can't verify.

- Also, look for additional red flags that may signal unethical practices when dealing with a cash buyer

At some point, you've probably seen a billboard or postcard advertising "We'll buy your house for cash!" The investors behind 'we buy houses' companies promise an all-cash offer on your home and a fast closing process. But is the promise legit?

If you need to sell fast or can no longer afford to maintain a property, selling to a 'we buy houses' company might actually be a good deal.

'We buy houses' companies generally purchase distressed properties at a bargain price. In many cases, they'll cover all or most of the closing costs and can settle the deal within 7–14 days.

Just keep in mind that an investor's ultimate goal is profit, so they're never going to offer you what they think your house could actually be worth.

Be sure to compare any offer against other options before accepting it — including listing with an agent. Good realtors can usually get you way more than a cash buyer would — even when you need to sell fast.

With Clever Offers, you can compare multiple offers from trusted cash buyers in your area against the sale price you'd get with an agent. Our service is free to home sellers, and there's no obligation to work with one of our investors. Simply tell us what you're looking for in an offer, and we'll do everything we can to help you explore your options and get the best possible deal for your home.

Are 'we buy houses' companies a rip-off?

Some people who've worked with 'we buy houses' companies complain that they're a rip-off or a scam — but it really depends on how you look at it.

If you're looking to get top dollar for your home, you're likely not going to get it from a 'we buy houses' company. But in a situation where you've fallen behind on your mortgage payments or can't afford the upkeep on a home that needs work, a fast cash offer might be your best option.

As a general rule, the investors behind 'we buy houses' companies won't pay more than 70% of the home's expected after-repair value — although some investors do pay more, depending on their investment strategy and the property itself.

If a home could be worth $140,000 on the real estate market after an $8,000 repair, an investor might try to offer $70,000–90,000.

So while selling your house to a cash buyer might not be a scam by itself, it could feel like a rip-off if you have better options on the table that could net you more money.

Is it ever a good idea to sell to a cash buyer?

"The only time you should sell to a cash buyer is when you have some reason when you need to handle it fast," says longtime investor Don Chambers. "With an agent, it's going to take six weeks, three or four months, maybe."

But if you have the time to list the house with an agent, a traditional sale is probably the way to go, says Chambers — even if the house needs work,

"If you get an agent and list it on the MLS, you're going to expose it to many more buyers. And when you get more buyers, you'll get a higher price."

⚡️ Compare cash offers to your home's ACTUAL value with Clever Offers.

Situations where selling to a 'we buy houses' company makes sense

There are a few scenarios where selling to a 'we buy houses' company may be a good option.

"Usually the sellers have inherited a home and don't live here. They just want to get it over with because they've got creditors to pay off and attorneys that are charging fees, and they just want to get everything settled," says Chambers. "That's the most common reason."

Sellers dealing with bad tenants or problematic rental properties, foreclosure situations, and privacy concerns (i.e., not wanting a lot of people coming in and out of the house) are other common reasons for seeking out a cash offer, the investor says.

| Good for | Bad for |

|---|---|

| Sellers who are facing foreclosure and/or have other debt problems | Sellers whose homes only need minimal prep and repairs before listing |

| Sellers with distressed properties that need significant repairs | Sellers in hot markets where houses easily sell as is |

| Sellers who have inherited a property and don't want to put any money into fixing it up and selling | Sellers who have a house that's already in good condition — the best value will be on the open market |

| Landlords dealing with bad tenants or wanting to offload a rental property without fixing it up | Sellers with the time and capacity to do a traditional listing, even if the house needs work |

In situations where selling to cash buyer makes sense, a legit 'we buy houses' company can typically offer:

- Speed: Legitimate cash buyers can close in as little as 1–2 weeks. In a traditional home sale, it takes 25 days, on average, to get an offer and another 30–45 days to close.

- Certainty: If a property is in very poor condition, lenders may not agree to finance a mortgage on it, limiting your buying pool to investors and bargain hunters willing to take on a project and pay cash. Investors can generally close on properties that other buyers would have trouble getting financing for.

'We buy houses' scams

Even though there are lots of legitimate cash buyers out there, scams do exist.

As a home seller, there are a few common cash-buying scams that you should be aware of:

- Email phishing: Someone sends an email to you with an all-cash offer and requests more information, like where to wire money. In the end, they end up using the information to access your account information and withdraw funds.

- Wholesaling: Someone puts your house under contract, and then tries to resell the contract to another buyer at a higher price. This is technically legal, but it can lead to trouble for the seller if the wholesaler is inexperienced and doesn't know what they're doing — for example, if they price the home too high and then can't find a buyer to take over the contract. Often, less ethical wholesalers try to include a clause in the fine print that allows them to walk away penalty-free if they can't find a buyer.

- Up-front fees: The cash buyer requests that you pay a fee or put down a deposit before they proceed with buying your home. You should never have to pay anything upfront, so don't! In all likelihood, the buyer intends to keep your payment and then cancel the deal.

- Equity skimming: A more elaborate scam in which the investor buys a property from a distressed homeowner, and then promises to let them buy it back when they're able. Instead, the investor refinances the home and takes out all of the equity.

- Foreclosure relief: The supposed buyer contacts a homeowner facing foreclosure and promises to negotiate with the bank to pay off mortgage delinquencies in exchange for an upfront fee. Instead, they take a few months of payments from the struggling homeowner, then break contact without ever speaking to lenders. The homeowner loses their home and the “rescue” fees paid to the investor.

Other red flags to watch out for when dealing with a 'we buy houses' company

A buyer who doesn't visit the property before making an offer

Igor Avratiner of We Buy Houses in Philadelphia advises caution if a buyer offers to purchase a property before actually seeing it and doing a home inspection.

"If an investor says they're going to have their inspector or contractor come out to evaluate the property after an agreement is signed, it's a good indication that they're going to try to lower their offer later on," says Avratiner.

Often, the inspector will find issues with the property and the buyer will try to re-negotiate with the seller at the last minute, hoping that the time and energy they've already invested will compel the seller to keep moving forward.

"All of this due diligence should be done before we sign a deal," says Avratiner.

Contingencies that let the buyer out of the contract late in the game or without penalty

Before signing anything, says Avratiner, "you really want to look at the contract, and you want to understand 'what are the contingencies?'"

Contingencies are clauses in a purchase contract that allow the buyer or seller to back out of a deal under certain conditions. Often, they protect buyers from having to follow through on a home purchase if a serious issue is discovered during an inspection or if they're unable to qualify for a loan due to underwriting or appraisal issues.

However, in the case of less ethical 'we buy houses' companies, contingencies can be abused.

Particular clauses to watch out for in a cash offer contract include:

- Statements indicating the buyer can cancel the agreement at any time or for any reason

- A closing date more than a few weeks out (buyers with cash shouldn't need more than 1–3 weeks to close)

- Clauses that allow the seller to relist the house while you're under contract

These contingencies may indicate that the buyer isn't actually intent on following through with the purchase. Instead, they may be trying to wholesale the deal under the table — meaning, they'll walk unless they can find another buyer willing to purchase the contract at a higher price.

Unwillingness to put down a significant deposit

According to Avratiner, an investor should typically put down 1-2% of the purchase price on a house when going under contract — the equivalent of $1,000–2,000 on a $100,000 house.

Buyers unwilling to risk this much earnest money may not be serious about following through on their offer.

As an example, Avratiner recently had a home seller reach back out to him after declining his initial offer. Another buyer had offered the owner $90,000 — about $40,000 more than Avrantiner thought the home was worth.

But at the end of the contract period, the original buyer threatened to cancel unless the owner agreed to take just $35,000 for the house — less than half the original offer price.

"He showed me the contract," says Avratiner, "and it contained a clause that said the buyer could cancel at any time and for any reason."

To make matters worse, the buyer had only put down a $100 in earnest money deposit — allowing them to walk away painlessly after stringing the seller along for more than a month.

Inability to show proof of funds

"If a buyer or wholesaler cannot provide proof of funds, stay far away from them," says Mike Bennett, a seasoned real estate investor and general manager of Clever Offers. "They are likely a novice and have little to no experience as an investor.

Proof of funds can come in the form of bank statements or a letter from a financial institution indicating the amount of funds the buyer has available.

Pressure to sign a contract before you've had it professionally reviewed

Just like with a standard real estate transaction, says Bennett, "sellers are advised to have legal counsel or a CPA review their contract before signing to ensure the seller is protected and has favorable terms."

"Some investors try to sneak in unfair contract terms like unreasonably long due diligence periods, low earnest money deposits, or clauses that can get them their earnest money back even if they cancel," explains Chambers.

A real estate attorney can spot loopholes that leave you unprotected and without compensation should the deal fall through. Buyers who try to get you to sign a contract before you've done this type of due diligence are a strong red flag.

How to protect yourself when working with a 'we buy houses' company

- When vetting a cash buyer, look for a professional website showing the names and contact information of the people you'll be working with, and positive customer reviews on sites like Google and the Better Business Bureau.

- Make sure the buyer has completed their inspections before accepting an offer. You can also ask them for a breakdown of how they arrived at their offer price.

- Ask the buyer for proof of funds and closing statements showing recent home purchases.

- Never pay a fee to a buyer — a legit investor will typically be the one to put down a deposit and cover the closing costs.

- Never feel pressured to accept an offer — especially before having it reviewed by an attorney or other professional you trust.

- Watch out for clauses in the contract that let the buyer out of the deal without forfeiting their earnest money deposit, which should typically be 1–2% of the offer price.

- Collect the earnest money deposit upon signing the contract — this should generally be wired to an escrow account set up through a title company or attorney.

- Perhaps most importantly, get competing bids before accepting an offer from a cash buyer and look over the contract terms (not just the offer price). Increasing the competition over your home is the best way to boost your sale price and ensure that a buyer is offering you a fair deal.

Compare multiple offers from trusted cash buyers in your area against the sale price you'd get with an agent. Clever Offers is free, and there's no obligation to accept an offer from our investors. Simply tell us about your property, and we'll do everything we can to get you the best possible offers for your home.

What customers say about 'we buy houses' companies

Reviews of some of the major cash-buying companies are mixed. That's probably because the pros and cons of working with a cash buyer really depend on your situation.

A low, all-cash offer might be a rip-off if you know you can get more on the open market, or it might be a life-saver if you need to sell the house quickly and get a little bit of money in your pocket.

For every negative experience that someone has with a cash buyer, there's an equally positive one, so you can't give too much weight to individual reviews.

Furthermore, there are thousands of companies and private investors that buy houses for cash, so there's bound to be a wide range in the quality of their service.

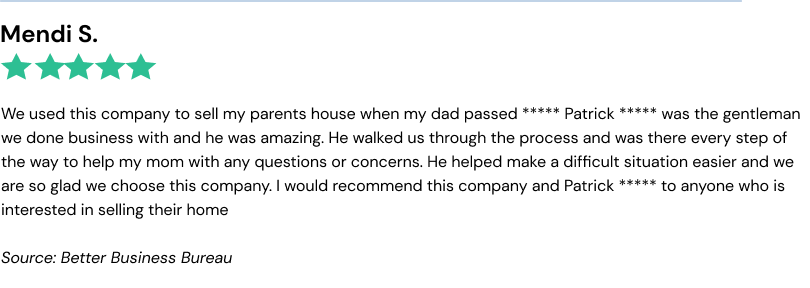

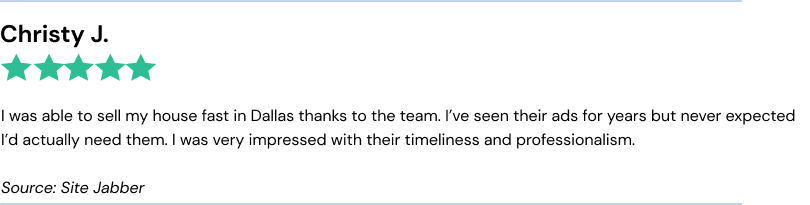

Positive experiences

Positive customer reviews of major 'we buy houses' companies like We Buy Ugly Houses and WeBuyHouses.com note how timely and convenient a service like this can be.

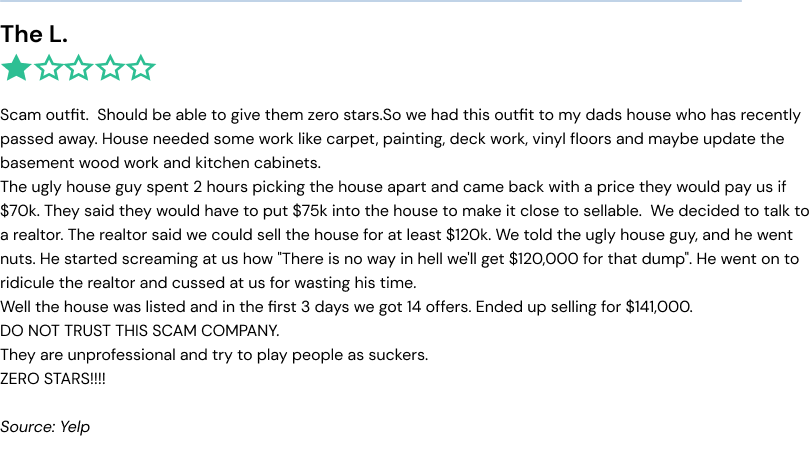

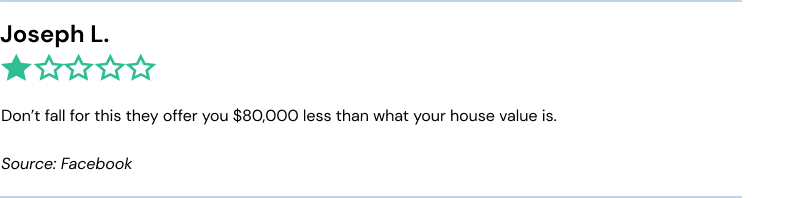

Customer complaints about 'we buy houses' ripoffs

Negative customer reviews primarily come from homeowners who complain that a "we buy houses" company offered them way less money than they expected for their homes.

Alternatives to using a 'we buy houses' company

If you want an all-cash offer from a buyer who can move quickly, selling to a "we buy houses for cash" company isn't your only option. You could:

- Sell to an iBuyer. iBuyers only operate in select markets, but they buy houses slightly below fair market value, do minimal repairs, and then sell them for a profit. If your home qualifies and doesn't need extensive repairs, this might be a good option since most iBuyers can close in as little as two weeks.

- Find a good real estate agent. If you're in a hot real estate market where homes are selling quickly, regardless of their condition, listing with the help of an agent might be the best way to get the most money for your home.

- Sell your house as is. With an as-is listing, the seller still lists their home on the open market, but with the caveat that they won't make any repairs or upgrades. What the buyer sees is what they get. An as-is sale might still net you significantly more than a 'we buy houses' company is willing to pay, and it could even attract the interest of an investor who will agree to close quickly.

FAQ

How do you know if a cash offer is legit?

If you get a cash offer, verify the company website or the buyer's identity, check for company reviews, and ask for proof of funds so that you can get a mortgage payoff letter from your lender. Before agreeing to make a deal, compare offers from multiple companies. to ensure you get a reasonable price. Don't let them rush you!

Are 'cash for houses' companies a rip-off?

A low offer from a company that advertises "cash for houses" might seem like a rip-off to some homeowners, but it really depends on your situation. Cash buyers almost always pay less than fair market value, but it might be worth it to you if you need to sell quickly and your home is in poor condition. If you have time, listing your home on the open market will almost certainly allow you to sell for a higher price.

Why is someone trying to buy my house?

"We buy houses" companies flip homes for profit. They'll often target older or distressed homes (owned by people in difficult financial situations) that they could buy for an affordable price. While it's legal to offer to buy a house for cash, these companies often make offers for far less than your home's actual value, hoping the homeowner is desperate and doesn't fully understand their options.